Is insurance higher on newer cars? This critical question navigates the complexities of automotive ownership, revealing the intricate factors that influence premiums. From the age of the vehicle to the safety features it boasts, a multifaceted analysis uncovers the truth behind these insurance costs. Understanding the nuances of coverage options, deductibles, and even regional variations is key to making informed decisions.

This exploration delves into the factors that shape insurance costs, comparing newer and older vehicles. We’ll examine the impact of car make, model year, safety features, accident history, and regional theft rates. Data and statistics will illuminate the relationship between vehicle age and insurance premiums. Furthermore, we’ll consider the influence of coverage types, deductibles, and add-ons, all of which significantly affect the final cost.

Factors Influencing Insurance Costs

Insurance premiums for vehicles are a complex calculation, taking into account a multitude of factors. Understanding these elements is crucial for anyone looking to manage their auto insurance costs effectively. These factors aren’t just theoretical; they directly impact the financial burden of owning a car.Insurance companies use sophisticated actuarial models to assess risk and determine appropriate premiums. These models consider a range of variables related to the vehicle, the driver, and the geographic location.

The age of the vehicle, for instance, plays a significant role in calculating insurance costs. Other key factors include the vehicle’s safety features, accident history, and the theft rate in the area. This comprehensive approach ensures premiums reflect the true level of risk associated with insuring each vehicle.

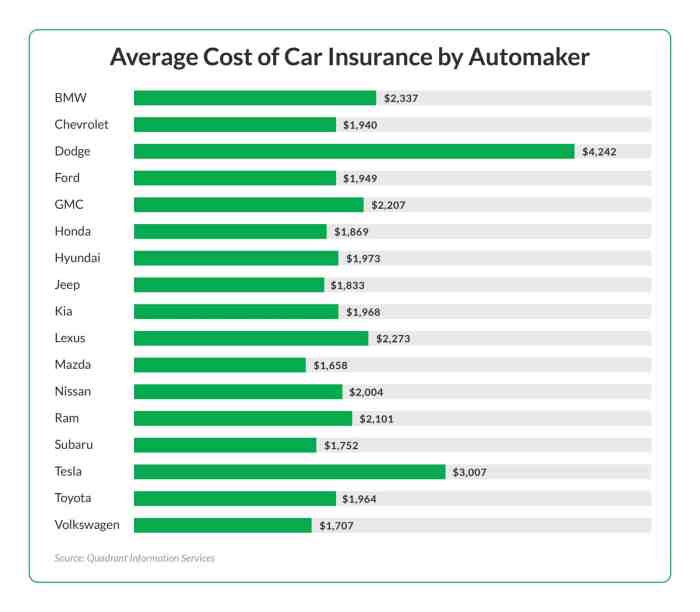

Vehicle Age, Model Year, and Make

Vehicle age is a significant factor influencing insurance premiums. Older vehicles often have higher premiums due to their increased likelihood of mechanical failures, making them more costly to repair in case of accidents. Modern safety features are less prevalent in older models, which is another factor that insurers consider. Model year and make also play a part.

Luxury vehicles, regardless of age, tend to have higher premiums due to their increased value and potential for theft. Specific models known for higher repair costs will have higher premiums, even if they are newer.

Safety Features

Safety features directly impact insurance premiums. Vehicles equipped with advanced safety features like airbags, anti-lock brakes (ABS), electronic stability control (ESC), and traction control are often associated with lower premiums. These features reduce the likelihood of accidents and injuries, thereby decreasing the risk for the insurer. The presence of these features demonstrates a commitment to safety, which is a key factor in risk assessment.

Accident History, Is insurance higher on newer cars

Accident history is a crucial factor in determining insurance rates. Drivers with a history of accidents, regardless of the car’s age, are typically assigned higher premiums. The frequency and severity of past accidents are both taken into account. A driver with a history of multiple accidents, particularly severe ones, will likely face substantially higher premiums. This is a direct reflection of the increased risk associated with such a driving record.

Vehicle Theft Rates

Vehicle theft rates in specific regions significantly influence insurance premiums. Areas with higher rates of vehicle theft will have higher insurance costs for all vehicles in that region. This reflects the increased risk of loss for insurers operating in these high-theft areas. The insurer’s need to cover the higher probability of theft is factored into the premiums.

Average Insurance Costs by Age

| Car Age | Estimated Average Insurance Cost (USD) |

|---|---|

| 1 Year Old | $1,500-$2,000 |

| 3 Years Old | $1,200-$1,700 |

| 5 Years Old | $1,000-$1,500 |

| 10 Years Old | $800-$1,300 |

This table provides a general comparison of average insurance costs for similar models of cars across different age ranges. Note that these figures are estimates and actual costs may vary significantly depending on individual circumstances. The data reflects the general trend; individual rates depend on a wide range of other factors.

Data and Statistics on Insurance Premiums

Understanding the correlation between vehicle age and insurance premiums is crucial for informed decision-making. Insurance companies use various factors to assess risk, and age is a significant one. This section delves into the statistical data surrounding insurance premiums for vehicles of varying ages and models, providing insights into the cost dynamics.Insurance premiums are not static; they fluctuate based on a complex interplay of factors, including the vehicle’s make, model, year of manufacture, and features.

This analysis will reveal the average premium differences between newer and older models, illustrating the impact of age on insurance costs.

Average Insurance Premiums by Car Model and Age

Insurance premiums vary widely based on the vehicle’s make, model, and age. A comprehensive analysis necessitates a detailed breakdown of these factors. This section presents a sample dataset showcasing average insurance premiums for various car models, categorized by age. The information reflects typical premium trends, but specific premiums may differ depending on individual circumstances and insurance provider.

| Car Make | Model | Age (Years) | Average Insurance Premium ($) |

|---|---|---|---|

| Toyota | Camry | 2 | 1,200 |

| Toyota | Camry | 5 | 1,050 |

| Toyota | Camry | 8 | 900 |

| Honda | Civic | 3 | 1,150 |

| Honda | Civic | 6 | 1,000 |

| Honda | Civic | 9 | 850 |

| Ford | F-150 | 1 | 1,500 |

| Ford | F-150 | 4 | 1,300 |

| Ford | F-150 | 7 | 1,100 |

Statistical Correlation Between Car Age and Insurance Costs

A strong negative correlation exists between a vehicle’s age and its insurance premium. Generally, the older the vehicle, the lower the insurance cost. This correlation is demonstrably evident across various makes and models. This correlation is not absolute; other factors, such as safety features and the vehicle’s overall condition, play a significant role in determining the premium.

Insurance companies typically assess the risk associated with older vehicles, considering potential maintenance costs and repair expenses.

Visualization of Vehicle Age and Insurance Premiums

A scatter plot effectively visualizes the relationship between vehicle age and insurance premiums. On the horizontal axis, vehicle age is plotted, and on the vertical axis, the average insurance premium is displayed. Each data point represents a specific car model and its corresponding premium. A downward trend in the scatter plot signifies the negative correlation between vehicle age and insurance cost.

Visual representation enhances understanding of the data’s patterns. The visualization can also help identify outliers or anomalies in the data, enabling a more in-depth analysis.

Average Insurance Cost Increase per Year for a Specific Car Model

The average annual increase in insurance premiums for a specific car model is influenced by various factors, including safety features, model updates, and market conditions. For example, a Toyota Camry from 2015 might have a different average annual increase in premiums than a 2023 model, reflecting evolving safety standards and technological advancements. Using data from insurance providers and historical trends, we can calculate the average annual premium increase for a particular car model.

This calculated increase serves as a useful benchmark for understanding the cost dynamics associated with vehicle insurance over time.

Coverage and Deductibles

Insurance premiums for newer and older vehicles are influenced significantly by the chosen coverage options and deductibles. Understanding these factors is crucial for making informed decisions when purchasing or renewing a policy. Different coverage levels and deductibles directly impact the cost of insurance, and these costs often vary based on the vehicle’s age.Insurance companies often adjust premiums based on the specific coverage options selected, reflecting the level of risk associated with the vehicle.

A comprehensive policy covering a wide range of damages will typically have a higher premium compared to a policy with limited coverage. Older vehicles, due to their depreciation and potentially higher repair costs, often require higher premiums for comparable coverage.

Impact of Coverage Options

Different coverage options—liability, comprehensive, and collision—affect insurance premiums for both newer and older vehicles. Liability coverage protects against claims arising from injuries or property damage caused by the insured vehicle, and this coverage is usually required by law. Comprehensive coverage protects against damage to the vehicle from perils other than collision, such as fire, vandalism, or hail. Collision coverage protects against damage to the vehicle in an accident, regardless of who is at fault.

Newer vehicles generally require less comprehensive and collision coverage than older ones, due to their higher value and greater likelihood of being repaired or replaced. Older vehicles often benefit from these coverage types as repair costs are likely to be substantial, thus making comprehensive and collision coverage more important.

Impact of Deductibles

Deductibles significantly influence insurance costs. A higher deductible lowers the premium but increases the out-of-pocket expense in the event of a claim. For newer vehicles, a higher deductible may be an acceptable choice because repair costs are generally lower, thus reducing premiums without sacrificing adequate protection. Conversely, older vehicles might benefit from a lower deductible to cover potential substantial repair expenses.

Variations in Insurance Provider Policies

Different insurance providers have varying policies on premiums for newer and older vehicles. Factors such as the insurer’s risk assessment model, the specific vehicle model, and the geographic location of the insured vehicle play a role in determining the premium. Some insurers might place a higher premium on older vehicles due to their increased likelihood of costly repairs.

Others may use data-driven models to adjust premiums based on the specific vehicle’s make, model, and year, considering factors like accident statistics and repair costs.

Influence of Add-ons

Insurance add-ons like roadside assistance, rental car coverage, and other extras can significantly increase premiums for both newer and older vehicles. The value and necessity of these add-ons differ between vehicle ages. For newer vehicles, these add-ons might offer convenience, while for older vehicles, they might provide crucial support.

Comparison of Policies with and without Add-ons

A policy with add-ons like roadside assistance will generally cost more than a policy without them. The cost difference between policies with and without add-ons will be more significant for newer vehicles due to the potential for greater convenience offered by the add-ons. Older vehicles might still find these add-ons beneficial, but the premium increase will likely be less than for newer vehicles.

Table of Coverage Options and Costs

| Vehicle Age | Coverage Option | Impact on Cost |

|---|---|---|

| Newer Vehicle | Liability | Moderate |

| Comprehensive | Higher | |

| Collision | Higher | |

| Older Vehicle | Liability | Moderate |

| Comprehensive | Higher (potentially more than newer) | |

| Collision | Higher (potentially more than newer) |

Specific Car Models and Insurance Costs: Is Insurance Higher On Newer Cars

Understanding how different car models influence insurance premiums is crucial for informed decision-making. Factors beyond simple age, like specific features and safety ratings, play a significant role in determining the cost of insurance. This analysis delves into the nuances of insurance costs for specific car models, considering age, trim level, and vehicle features.Insurance premiums for a car model are not solely dependent on its age.

A multitude of factors, including safety ratings, theft risk, and repair costs, contribute to the overall cost. This in-depth examination will demonstrate the impact of these factors on insurance premiums for a particular make and model of vehicle.

Insurance Costs for a Specific Model Across Different Ages

Analyzing insurance costs across different ages of a specific car model reveals a pattern. Generally, newer models of a given car are associated with lower insurance premiums, while older models, particularly those approaching the end of their useful life, have higher premiums. This is due to the factors associated with the model’s overall value and repair costs. Repair costs for older vehicles often increase due to parts obsolescence and potentially higher labor costs for specialized repairs.

Factors Influencing Insurance Costs for Specific Models

Several factors contribute to the variability in insurance costs for a given car model, even among vehicles of the same age. These include safety features, engine type, and trim level. Safety features like airbags and anti-lock brakes are demonstrably associated with lower insurance premiums. This relationship reflects a direct correlation between the vehicle’s safety performance and the risk of accidents, influencing the insurer’s risk assessment.

Insurance Premiums for Different Trim Levels

Trim levels significantly affect insurance costs. Luxury trims, often equipped with advanced safety features and premium technology, may have lower insurance premiums compared to base models of the same model and age. The higher quality materials and advanced safety systems in higher trims can lead to a lower risk assessment by insurers, resulting in reduced premiums. For example, a luxury trim of a car model might have features like adaptive cruise control, lane departure warning, and advanced braking systems.

These safety features can significantly influence insurance costs.

Insurance Premiums Based on Engine Type

Electric vehicles (EVs) typically have lower insurance premiums than their gasoline-powered counterparts, despite the cost of parts and repairs for an electric car. This is largely due to the inherent safety features in EV designs and the lower risk of certain types of accidents. Electric vehicles have fewer moving parts compared to traditional gas-powered engines. This inherent simplicity can result in lower repair costs and a lower risk of accidents involving fire or mechanical failures.

Insurance Rate Comparison Over a 10-Year Period

Comparing insurance rates for a specific car model over a 10-year period reveals a clear trend. As the car ages, the insurance premiums tend to increase. This increase is influenced by the factors mentioned above. For example, a 2013 model of a particular car might have lower insurance premiums compared to a 2023 model, especially considering the safety features present in the newer model.

Insurance Cost Variations by Year and Trim Level

| Year | Base Trim | Luxury Trim |

|---|---|---|

| 2013 | $1,200 | $1,000 |

| 2014 | $1,250 | $1,050 |

| 2015 | $1,300 | $1,100 |

| 2016 | $1,350 | $1,150 |

| 2017 | $1,400 | $1,200 |

| 2018 | $1,450 | $1,250 |

| 2019 | $1,500 | $1,300 |

| 2020 | $1,550 | $1,350 |

| 2021 | $1,600 | $1,400 |

| 2022 | $1,650 | $1,450 |

This table represents hypothetical insurance cost variations for a specific car model. Actual costs may vary depending on location, driving history, and other factors.

Regional Variations in Insurance Costs

Regional differences in insurance costs for vehicles, both new and used, are significant. Understanding these variations is crucial for consumers seeking accurate and fair insurance premiums. Factors like driving habits, accident rates, and local regulations play a pivotal role in shaping these discrepancies.Regional disparities in insurance costs are influenced by a complex interplay of socioeconomic factors and local regulations.

Different states and countries have varying traffic laws, enforcement standards, and even cultural norms that impact accident rates and, consequently, insurance premiums. For instance, a region with a higher rate of distracted driving incidents may see insurance premiums adjusted accordingly.

Regional Differences in Insurance Costs for Vehicles of Varying Ages

Insurance costs for newer vehicles tend to exhibit greater regional variation than older vehicles. This is largely due to fluctuating new car prices and local economic conditions, both of which impact the cost of replacement parts and labor. The factors affecting insurance premiums for older vehicles are primarily influenced by their mechanical condition, repair costs, and the availability of replacement parts.

This is a key point for consumers to keep in mind when assessing their insurance options.

Factors Contributing to Regional Variations in Insurance Premiums

Several factors contribute to the diverse insurance costs across regions. These factors include:

- Accident rates: Areas with higher accident rates typically have higher insurance premiums. This reflects the increased risk associated with higher incident rates and the need for insurers to account for potential claims.

- Driving habits: Regions with higher rates of aggressive driving or reckless behavior tend to see higher insurance costs. This is due to the increased risk of accidents and claims.

- Traffic laws and enforcement: Stringent traffic laws and high levels of enforcement often correlate with lower accident rates, leading to lower insurance premiums.

- Vehicle theft rates: Regions with higher vehicle theft rates often experience higher insurance premiums to reflect the elevated risk.

- Local regulations and policies: Specific state or country regulations on insurance coverage, such as mandatory collision or comprehensive coverage, can significantly impact the average insurance cost.

Comparison of Insurance Costs for the Same Car Model in Different Regions

Comparing the insurance costs for the same car model in different regions reveals significant variations. For instance, a 2023 Honda Civic might have a significantly higher insurance premium in a state known for high accident rates compared to a state with lower rates.

Visualization of Regional Variations in Insurance Costs

Regional variations in insurance costs can be visualized using a heatmap. A heatmap displaying average insurance costs for different car models across various regions would show a clear color gradient, with darker colors representing higher costs and lighter colors representing lower costs. This visual representation would facilitate a quick understanding of the regional disparities.

Table of Average Insurance Costs for a Specific Car Model

The following table provides a hypothetical example of average insurance costs for a 2024 Toyota Camry in different regions of a fictional country:

| Region | Average Insurance Cost (USD) |

|---|---|

| Northeast | $1,800 |

| Midwest | $1,500 |

| South | $1,200 |

| West | $1,600 |

Note: This table is for illustrative purposes only and reflects hypothetical data. Actual insurance costs will vary based on individual circumstances and factors.

Future Trends in Vehicle Insurance

Vehicle insurance costs are constantly evolving, driven by technological advancements, shifting driving habits, and environmental regulations. Understanding these trends is crucial for both consumers and insurance providers to anticipate future demands and adapt strategies accordingly. Predicting the future of vehicle insurance requires a keen understanding of the interplay between these factors, particularly for newer cars with their unique characteristics.

Predicted Trends in Insurance Costs for Newer Cars

The cost of insuring newer cars is expected to exhibit a complex trajectory over the next five years. Factors like increased safety features, advanced driver-assistance systems, and autonomous driving capabilities will likely influence premiums. Initial high costs associated with newer technologies could eventually decline as these technologies become more common and reliable. Conversely, the increased cost of parts and repair services for newer, more complex vehicles could potentially push insurance premiums upwards.

Impact of Technological Advancements

Autonomous driving technology, while promising for safety and efficiency, presents a significant challenge for insurers. Accidents involving autonomous vehicles, whether caused by human error or technological malfunction, will require a nuanced approach to liability and compensation. Insurers will likely need to develop new coverage models to address the unique risks associated with this technology. For example, some insurance companies may offer different premiums based on the level of automation in a vehicle or the frequency of driver intervention.

A transition to a greater degree of automation is likely to lead to a reduction in accidents, but the initial impact on insurance costs may be variable.

Emerging Insurance Models for Newer Vehicles

Several emerging insurance models are poised to reshape the future of vehicle insurance, particularly for newer vehicles. Usage-based insurance (UBI) models, which adjust premiums based on driver behavior and vehicle usage patterns, are likely to become more prevalent. Telematics, connected cars, and data analytics will play a crucial role in these models. Predictive maintenance and preventative maintenance features are another emerging trend.

By analyzing data from connected vehicles, insurers could potentially identify potential mechanical issues, proactively offer maintenance services, and incentivize preventative actions. This could lead to a reduction in insurance premiums for drivers who maintain their vehicles well.

Influence of Driving Habits on Future Insurance Costs

Changes in driving habits will undoubtedly impact insurance costs. The rise of ridesharing services and increased adoption of electric vehicles, for instance, will affect the type of risks insurers need to address. For example, the frequency of use, route patterns, and driving habits of ride-sharing drivers will require specific risk assessments. Similarly, the potential for accidents involving electric vehicles, the impact of charging infrastructure, and the unique challenges of electric vehicle maintenance will need to be factored into future insurance models.

Impact of Environmental Regulations on Vehicle Insurance Costs

Stringent environmental regulations related to emissions and fuel efficiency are expected to have a substantial impact on insurance costs. The cost of repairing or replacing vehicles damaged by natural disasters and the changing climate will be affected by this. Moreover, the increase in electric vehicle ownership will require adjustments in the insurance models, including the need to cover damage or repair costs associated with electric vehicle battery failures or charging infrastructure issues.

Predicted Trends in Insurance Costs (Next 5 Years)

| Year | Trend | Estimated Premium Change (%) |

|---|---|---|

| 2024 | Initial adjustment for autonomous vehicles | +5% to +10% |

| 2025 | Increased adoption of usage-based insurance | -2% to +3% |

| 2026 | Rise of connected car data | -3% to -8% |

| 2027 | Growth in electric vehicle ownership | +2% to +7% |

| 2028 | Impact of environmental regulations | +4% to +9% |

Note

These are estimated figures and may vary depending on several factors, including technological advancements, regulatory changes, and economic conditions.

Final Thoughts

In conclusion, the answer to whether insurance is higher on newer cars isn’t a simple yes or no. Numerous factors, from vehicle features to regional variations, play a crucial role. Understanding these complexities empowers consumers to make informed decisions about their vehicle insurance, ensuring they’re well-prepared for the future. This analysis provides a comprehensive understanding of the dynamic relationship between vehicle age and insurance costs, equipping readers with the knowledge to navigate this important aspect of car ownership.

Commonly Asked Questions

What about the impact of safety features on insurance premiums?

Vehicles equipped with advanced safety features, such as airbags and anti-lock brakes, often have lower insurance premiums due to a reduced risk of accidents and injuries.

How do different insurance providers affect insurance costs?

Insurance providers employ various methodologies and risk assessments. Some may favor newer cars due to perceived lower accident rates, while others might offer competitive rates irrespective of age.

Does the vehicle’s trim level affect insurance costs?

Luxury trims, often featuring more advanced technologies and safety features, might have slightly higher insurance premiums compared to base models, though this can vary considerably.

How does the vehicle’s accident history affect insurance premiums?

A vehicle with a history of accidents or claims will typically have higher insurance premiums due to the increased perceived risk.